Reader Question: My home is paid for and recently went up for sale (375k). I want to buy another home in the neighborhood (420k). How can I do this before my present home sells? I do not want to miss out on the other home. Thanks, Robyn.

Reader Question: My home is paid for and recently went up for sale (375k). I want to buy another home in the neighborhood (420k). How can I do this before my present home sells? I do not want to miss out on the other home. Thanks, Robyn.

Monty’s Answer: Hello Robyn, thanks for your question. If a loan is needed to buy the second home now, you must get the money from a lender like a bank, credit union or online lender. Your income, assets, and obligations will play a role in gaining loan approval. There is an article on DearMonty.com entitled finding the right mortgage to get started. Arranging a home loan today takes time. Your “free and clear home” status should help to get quick approval. A faster source for financing may be the owner of the other home. Depending on their reason for selling and their financial situation, they have a motive for granting a loan and could be a source of funds.

Is there enough income to hold a second home comfortably until it sells? Is there other savings to make a down payment on the new one? Will a lender fund a loan without encumbering your original home? One possibility may be using part of the equity in the old home for the down payment on the new one and then pay off the equity loan when the old home sells. Knowing the market well enough to predict how long and at what price you can expect a sale will be helpful in making the right decision.

Preventing an unhappy ending.

I once knew a family that found a home they loved. The agent told them their old home would sell for $225,000 within 60 days. On the strength of that statement, they went ahead and bought the new house. The result was the home took 2 years to sell, and sold for $150,000. In the end, the financial strain of owning and caring for two homes and the time-on-market compromised their negotiating power. Neither buyer nor agent wants to end up in this position. There is a way to reduce the chance of this happening. Read on to learn more.

Gather the right data.

Certain parts of the country are burdened with foreclosures, bank owned homes and shadow inventory of pre-foreclosure properties. In some areas, property values are on the rebound. Your real estate agent can furnish all the comparable sales over the past 3 years. They can share the data sheets of properties directly competing with your current home for future buyers. They also know how many similar homes came on the market from this time forward for the last 3 years. This information provides a sense for what can be expected this year.

Evaluating the risk.

Knowing the number of similar homes currently for sale or coming for sale and the number that sell annually will allow you to calculate the sales rate. For example, if 20 homes like yours sell each year and there are 300 either for sale or expected to come up for sale based on the prior years, this snapshot suggests that today there is a 15 years supply. 300 for sale/20 sales equal 15 years to diminish the supply. Conversely, if there are 20 similar homes for sale or expected to come on the market and history shows 20 will sell, these numbers suggest the supply is 1 year or less. While this methodology is being applied to a moving target, there are much better odds of completing a sale sooner and at a higher price in the second example.

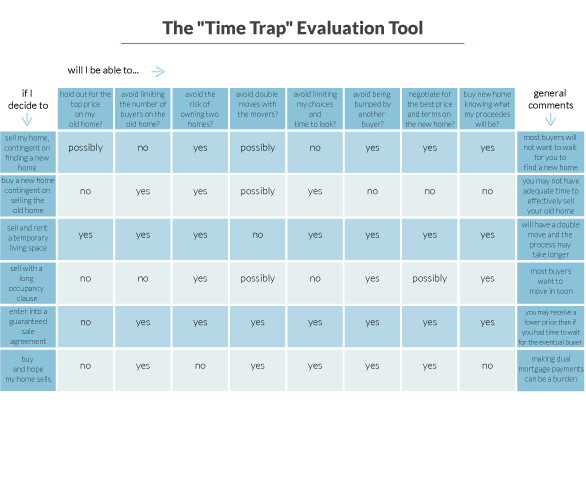

An article on DearMonty.com titled “Risk evaluation of owning two homes” provides additional possibilities to consider. This information may help in making a sound decision.

I hope this information is helpful, Robyn. Ask me if you have other questions.

Respectfully,

Monty

Leave a Reply

You must be logged in to post a comment.